Applying Nelson's formula to a modern grant

Stock-grant structures have changed materially in the 40 years since Marriage of Nelson (1986): the original equation, written for a single-event cliff, cannot be applied directly to modern multi-tranche grants. Every method in current use is therefore some adaptation of it. Vest-Level Nelson is one such adaptation; it is not the law as written.

"In contrast, the trial court here utilized a formula in which the numerator was the number of months from the date of grant of each block of [shares] to the date of the couple's separation, while the denominator was the period from the time of each grant to its date of exercisability."

In Nelson's formula, the bolded references all point to the same object: a block of [shares] with one grant date and one date of exercisability — one equation, applied once. Current practice instead replaces each block-reference with a tranche-reference (underlined in red below) and sums dozens of such equations together. That sum is not mathematically equivalent to Nelson's: there is only one grant date per grant, so the same date is reused as the start of every summed fraction, double-counting the grant's earning period and producing a curve rather than a line. Employers who want parallel earning issue parallel grants.

"In contrast, the trial court here utilized a formula in which the numerator was the number of months from the date of grant of each tranche of shares to the date of the couple's separation, while the denominator was the period from the start of each tranche of shares to the tranche of shares date of exercisability."

For grants in the original Marriage of Nelson case, "date of exercisability" and "date of grant completion" were identical. The natural extension to a multi-event grant uses the latter:

"In contrast, the trial court here utilized a formula in which the numerator was the number of months from the date of grant of each block of [shares] to the date of the couple's separation, while the denominator was the period from the time of each grant to the date of grant completion."

This substitution is equivalent to what a monthly ratable vesting schedule already delivers, as can be seen by visual inspection — the grant treated as a single unit with a date of grant, a date of completion, and the months of community service in between.

The vesting schedule is the employer's intended earning curve

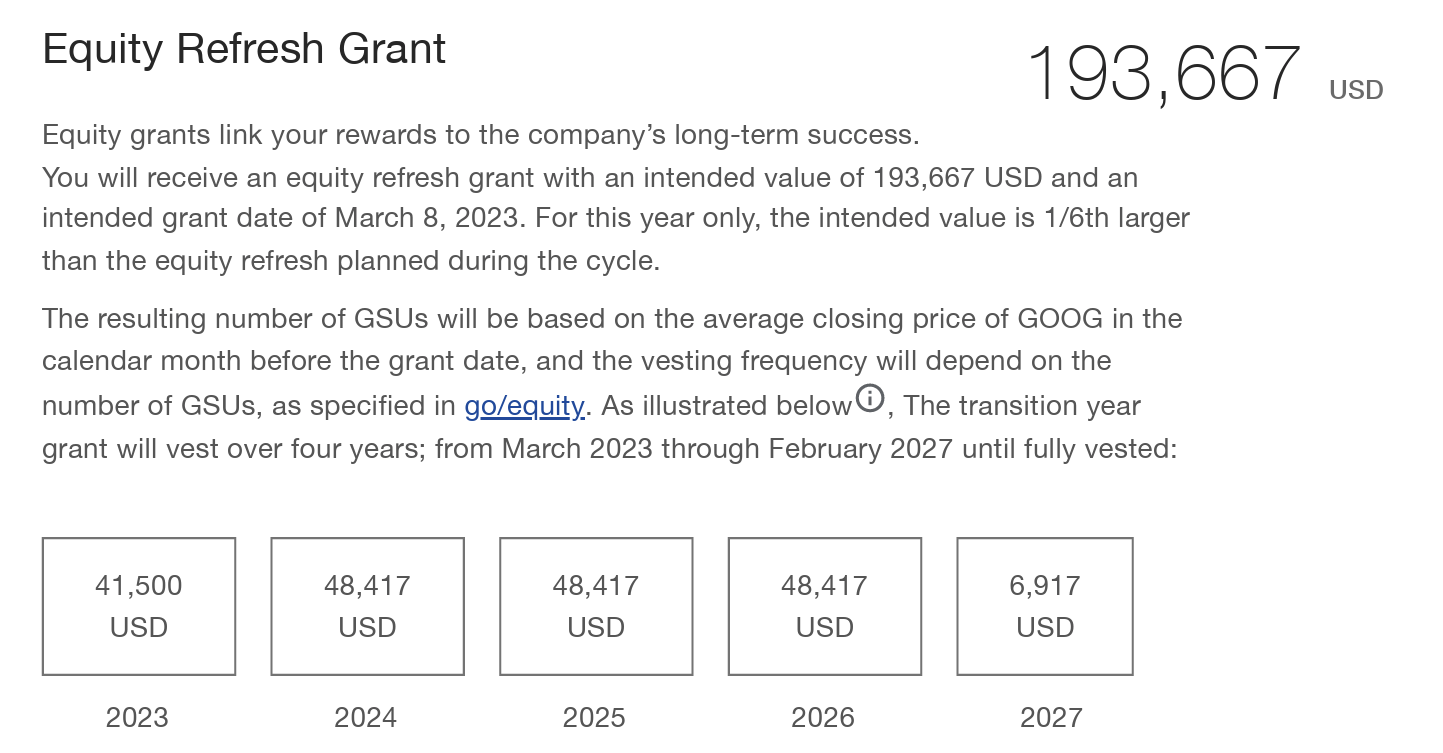

The Alphabet equity refresh grant below (Image 1) shows a refresh grant as a singular object — one dollar value earned ratably over a 4-year period, economically equivalent to a $48,417/yr deferred salary supplement (paid in shares to motivate the employee to drive the company's success). The rate at which the ratable shares are released is determined solely by the number of shares issued, which varies with the stock price. If an employer wants earning to be front-loaded, they design the vesting schedule as such — as in the respondent's initial Alphabet grant (Image 2).

Both shapes are deliberate design. The next page examines what happens when an apportionment formula imposes a different curve on top.

Cadence is a distribution choice — not a measure of value

Like cash paid in installments, the grant accumulates fraction by fraction — earning at any analysis date cannot exceed the cumulative paid through the next scheduled vest. Meta's plan documents the constraint:

"Form and Timing of Settlement. Payment of earned RSUs shall be made as soon as practicable after the date(s) determined by the Committee and set forth in the Award Agreement."

Vest-Level Nelson violates this constraint — and the magnitude of the violation swings sharply with vesting frequency. Alphabet's plan treats frequency as a distribution variable only, tied to share count — not to how the value is earned. The chart below shows a single grant at the 50% separation point under three cadences: only the cliff respects the cap (one eventual tranche, formula needed); any multi-tranche schedule overshoots. Same dollar grant, same period, same time worked — only the vesting frequency differs.

At 50% separation, the date itself coincides with a scheduled vest, so the schedule has delivered exactly 50% of the grant. Vest-Level Nelson's 79% (annual) and 84% (monthly) claims overshoot the cap, claiming shares the schedule has not paid.

Concrete example: Google's 20-for-1 stock split on July 18, 2022. Two employees hired with the same dollar grant value — one immediately before, one immediately after — receive share counts differing by 20×. Per Alphabet's plan, share count drives vesting frequency, so the 20× gap can place the two in different cadences — and Vest-Level Nelson can then produce different community claims, despite identical grants, terms, and time worked. Identical earnings, different Vest-Level Nelson claims — because the method tracks the distribution frequency, not how the compensation is earned.

Visual comparison of accumulated shares

Both grants and yearly salary are deferred compensation paid over a period of year(s), settled in periodic distributions — vests and paychecks. The periodic structure exists for the same reason in both: it limits the holder's forfeiture risk by paying as work is performed. The four panels below trace how each accumulates: Nelson's original result (green), a yearly salary (purple), and the Vested Shares Method (blue) all share the same time-apportioned shape; Vest-Level Nelson (red) diverges.

Ongoing complexity that extends the dissolving relationship

Unlike the other solutions discussed, Vest-Level Nelson requires a significant number of joint calculations — pricing the shares, splitting the community portion, reconciling withholding, adjusting support. These must be ratified into the divorce settlement, then settled by both parties on their own once the orders are in place, often across multiple grants pushing the total above 100. The same calculations factor into support: community shares later appear on the employee's W-2 as ordinary income and must be excluded from support income to prevent double-counting — a common place for accounting error.

The Vested Shares Method, by contrast, requires no post-decree calculations — the community owns its share at separation, and allows the marriage to end at the settlement agreement.

This case — applying the methods to the actual grants

Computed at the marriage date (2021-06-15) and a representative date of separation (2024-02-29) chosen between the dates argued by the parties. The methodology argument is independent of which DOS prevails — only the magnitude of the over-allocation changes. Share values use each party's current stock price; grants issued after separation or completed before the marriage are excluded.

Earning rate going forward — shares retained per month of continued work

Each card shows the post-decree take-home rate from a holder's own grants — what each party retains per month of continued work. Cross-party community shares are not netted: each holder keeps their half of the other's community whether they continue working or not.

These rates assume both parties remain employed. If one leaves their position, future vests on their grants cease — removing one side of the cross-flow that partially offsets Vest-Level Nelson's transfer. The party who remains employed continues to owe a portion of every future vest with no balancing flow back, falling hardest on whichever party stays in their role longest. The support-calc reduction is roughly twice the take-home reduction: the full community portion must be excluded from support income, not just the half that transfers to the other party.

The shares that actually vested during the marriage are the community's share

The purpose of the time-rule established in Marriage of Nelson (1986) was to apportion stock-grant value in proportion to time worked. Modern monthly-ratable vesting already does exactly that — the employer has written the apportionment into the grant itself, distributing shares in the same proportional shape the Nelson court derived by formula. The formula is not needed a second time, on top of the schedule that already produces it.

Applying an additional per-tranche formula on top of that schedule imposes a steeper, front-loaded curve; requires years of post-decree reconciliations the parties must calculate and complete; opens a persistent source of error in spousal and child support; overrides the employer's own stated design for each grant; and — as the case-impact page showed — shifts substantial value out of each party's separate property into the community pot that the Vested Shares Method would not.

This is the Vested Shares Method. It produces the Nelson result, it requires no post-decree administration, it avoids the double-counting trap in guideline support, and it honors the employer's design as written. The pages above show the curves, the case-specific impact on this matter, and the operational and legal consequences of departing from that design.

Earnings at 25%, 50%, and 75% separation

Three snapshots of the same grant — at 25%, 50%, and 75% separation. On a monthly ratable schedule, the percent vested matches the percent elapsed: 25% / 50% / 75%. Vest-Level Nelson credits more in every case (59% / 84% / 96%) — and the most, relative to what's actually vested, at the earliest separation.

Year-by-year earning rate — three separation points on one chart

Each bar is one year of vesting. Nelson and monthly ratable produce a consistent year-to-year earning rate. Vest-Level Nelson's earning rate drops drastically — from 59% in Year 1 to just 4% in Year 4, a 94% drop — materially distorting the employee's available income even though the grant pays the same rate every year.